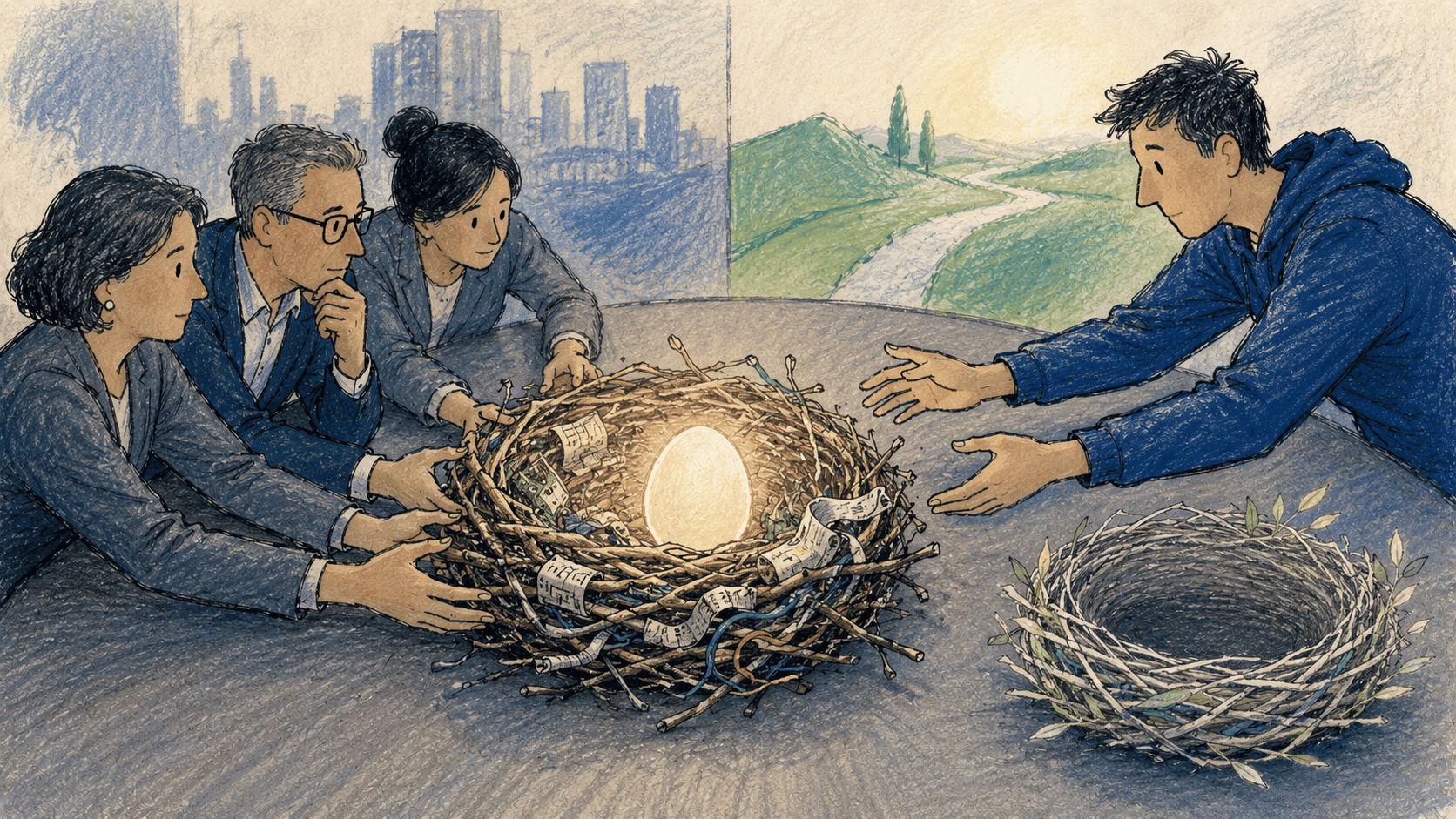

Investors and the New-Company Question

Many founders eventually hit the fork in the road. The original plan is grinding, and a bigger, cleaner opportunity is suddenly in view. The question that follows is deceptively simple: do we pursue this inside the company we already have, or do we start a new one?

I’ve watched founders treat this as a product decision. It isn’t. It’s a governance and ownership decision, and it is one of the few moments in a startup’s life where the founder’s interests and the investors’ interests can pull hard in opposite directions. If you don’t see the second set of interests clearly, you can blow up relationships, trigger legal exposure, and torch your reputation in a small ecosystem that has a very long memory.

This post is written founder-to-founder, but its real purpose is to get you to sit in your investors’ chair for a few minutes. Pivots feel like progress to you. To the people who funded you, they can feel like the prize walking out the door. Understanding why is how you make a decision you won’t regret.

The Core Tension in One Line

Strip away the lawyers and the term sheets and you’re left with two rational actors optimizing for two different things.

Founders optimize for future opportunity value and strategic freedom.

Investors optimize for ownership continuity of the value their capital created.

Neither side is the villain here. Both positions are legitimate. The conflict comes from the fact that a pivot can increase total value while changing who owns it — and that redistribution is exactly what your investors are watching.

Here’s the same tension as a 2×2.

| Keep It in the Existing Company | Start a New Company | |

|---|---|---|

| Founder’s instinct | Preserve assets, cash, team, and momentum | Reset equity, escape bad terms, get a clean brand |

| Investor’s instinct | Protect and leverage the investment they already made | Only if the old business is truly dead — and only with participation rights |

Founders tend to live in the right-hand column. Investors live in the left. That gap is the whole ballgame.

What the Pivot Looks Like From the Other Chair

It helps to be explicit about both sides before we go deeper. Here is the honest ledger.

| Keep Existing Company | Start New Company | |

|---|---|---|

| Founder upside | Keep the cash, cap table, contracts, IP, customers, and brand. Avoid legal and setup costs. Fundraise as “evolution,” not “failure.” | Clean cap table, reset ownership, escape liquidation preferences and governance constraints, recruit on fresh equity, no legacy baggage. |

| Founder downside | Legacy investors own upside they didn’t fund the new version of. Old preferences and board rights still bind you. Prior valuation can anchor the next round. | Disputes with existing investors, possible fiduciary-duty claims, rebuilt infrastructure and relationships, IP ownership questions, reputation risk. |

| Investor upside | Their ownership rides the new opportunity. Diligence, trust, and reserves are already in place. Lower friction. | Cleaner economics if the old business is dead; they can choose whether to back the new risk profile. |

| Investor downside | Capital raised for one thesis now funds another; harder to judge against the original case; more follow-on may be required. | They can lose access to the upside entirely while their funded learning, IP, and talent walk out the door. |

Read that bottom-right cell again, because it is the one founders gloss over. The worst-case outcome for your investor is the one your “clean new company” plan creates.

“Who Owns the Opportunity?” Is a Real Legal Question

Most founders assume that an idea in their head belongs to them. In the eyes of corporate law, that assumption is not safe — and your investors know it even if you don’t.

The relevant concept is the corporate opportunity doctrine. As an officer and director, you owe a fiduciary duty to the company. If a business opportunity comes to you that is in the company’s line of business, that the company could pursue, and in which it has an interest or expectancy, you generally have to offer it to the company first. You can’t simply scoop it for yourself.

This isn’t theoretical. It’s the law that built Pepsi’s modern owner.

In Guth v. Loft (Delaware, 1939) — the case every corporate law student reads — Charles Guth was president of Loft, a candy and syrup company. He acquired the Pepsi-Cola opportunity personally, but he used Loft’s money, facilities, and employees to do it. The Delaware court imposed a constructive trust: Pepsi belonged to Loft, not to Guth, precisely because he developed it with the company’s resources while running the company. (case summary)

The doctrine isn’t a trap that catches every pivot, though. The same courts drew the line in the other direction in Broz v. Cellular Information Systems (Delaware, 1996). A director personally bought a cellular license and was found not liable — because the company lacked the financial ability and the interest to pursue it, and the opportunity had come to him personally. The court explicitly said there is no per se rule requiring you to present every opportunity to the board. (case summary)

Put those two cases side by side and you have the test your investors will apply.

| Factor | Points toward “company owns it” (Guth) | Points toward “founder owns it” (Broz) |

|---|---|---|

| Resources used | Company money, staff, IP, or data | Developed independently, on your own time |

| Line of business | Same or adjacent to the company’s mission | Genuinely unrelated |

| Company’s ability | Company could realistically pursue it | Company has no means to pursue it |

| Board process | Never disclosed; surfaced later | Formally presented and declined |

The more your situation looks like the left column, the stronger your investors’ claim — moral and legal — that the opportunity belongs inside the company, or that they at least deserve a piece of it.

What Investors Actually Fear

Investors are not afraid of pivots. Good ones expect pivots; they back teams precisely because teams find new paths. What they fear is a specific sequence:

- The founder discovers a much larger opportunity.

- The discovery happens on company time, using company employees, customer conversations, and capital.

- The founder concludes the new thing is more attractive than the old thing.

- The founder launches it as a new, personally-owned company.

- The original investors are left holding the dying business they funded.

From their seat, it reads as one sentence: “We funded the exploration, and the founder kept the prize.” Even when you have no such intent, a poorly handled pivot can look exactly like this from the outside. Perception alone is enough to break the relationship.

The Downsides You Need to Sit With — for Three Parties

You asked your investors to take a risk on you. The least they’re owed is that you understand who absorbs the damage when a pivot is handled badly. There are three victims, not one.

The downside to your investors. Their capital was allocated to a specific thesis; a pivot quietly redirects it to a different one they never underwrote. If you spin the new opportunity into a separate entity, they can lose access to the upside entirely while the learning, IP, and key people they paid for walk out the door. Even in a clean internal pivot, they may face larger follow-on requirements and lose any clean way to judge the investment against the case they originally bought.

The downside to you, the founder. This is the part founders underestimate. Spinning out to “escape” your cap table can trigger fiduciary-duty claims, asset-ownership fights, and a reputation as someone who walked away from the people who backed them. Venture is a repeat game played in a small room. The investors you stiff on this deal talk to the investors you’ll pitch on the next one. A messy spinout can cost you far more in future access to capital than you ever saved on equity. And if you keep the pivot inside the old entity, you carry the old preferences, the old board rights, and a valuation history that can anchor your next round downward.

The downside to the startup(s) themselves. A pivot splits founder attention, and split attention is how both the old and new businesses underperform. Value gets stranded: customers, contracts, and institutional knowledge sit in one entity while the energy moves to another. IP ownership becomes ambiguous exactly when you can least afford ambiguity — during diligence on your next raise. The cleanest-looking spinout on a whiteboard is often the one that leaves the most value bleeding out on the floor.

Three Real Endings

The theory lands harder with real outcomes. Here are three founders who hit this exact fork and handled the investor question very differently.

Odeo → Twitter: the investors sold the prize. When Apple’s podcasting push gutted Odeo’s original business, Evan Williams bought the company back from its VC (Charles River Ventures) and angels — including the twitter.com assets — for roughly $5 million. The investors were made whole and common holders took a modest gain, so this was fairly done. But the side project he carried out became Twitter. Five years later those assets were worth on the order of 1,000x what the investors sold them for. (TechCrunch) The lesson cuts both ways: the founder did the honorable thing by buying them out, yet the investors who let the vehicle go missed a generational outcome. When the opportunity and the entity get separated, someone is on the wrong side of that table.

Glitch → Slack: keep them whole and in the upside. Stewart Butterfield’s game Glitch was failing with about $6 million left of the $15 million he’d raised. He called his investors and offered to simply hand the remaining cash back. Instead, he pitched the internal chat tool his team had built — and his investors, trusting the team, stayed in the same company. That company became Slack, acquired by Salesforce for $27.7 billion. (Startup Archive) The pivot was radical; the ownership continuity was preserved. Investors rode the new opportunity because the founder kept them inside the tent.

Burbn → Instagram: the internal pivot done right. Kevin Systrom’s check-in app Burbn was going nowhere, but its photo feature was the only thing users loved. He stripped the app down to photo sharing inside the existing entity. The same investors who backed Burbn rode Instagram to its $1 billion sale to Facebook eighteen months later. No new entity, no dispute, no orphaned upside.

Notice the pattern. The pivots that preserved trust kept the investors’ ownership riding the new opportunity. The one that separated entity from opportunity left value on someone’s side of the table — even when the founder behaved well.

The Spectrum of Clean Outcomes

You don’t have to choose between “trapped in the old company” and “burn the investors.” There’s a spectrum, and the middle is where most good outcomes live.

| Structure | What investors get | Best when |

|---|---|---|

| Internal pivot | Full continuity of ownership | New business extends the mission; existing assets are material |

| Spinout with shared ownership | Equity, warrants, royalties, or IP license in NewCo | Opportunities are related but genuinely distinct |

| Board waiver | A clean, documented decision | Board formally declines; founder wants legal clarity to leave |

| Investor participation rights | Pro-rata or preferred access to invest in NewCo | A different investor base fits, but you want to keep faith with current backers |

| Clean new company | Nothing (highest risk) | The old business is truly dead and resources were genuinely not used |

If you take one structural idea from this post, take this: whenever you can, keep your existing investors riding the new upside. It is the single move that converts a potential fight into continued partnership.

The Test to Run Before You Decide

Before you call a lawyer or a co-founder, run the opportunity through one honest question — the same one an independent third party (or a judge) would ask:

If an outsider examined how this opportunity was discovered, would they conclude it arose from company-funded resources — your time as CEO, your team, your customers, your capital, your data?

The more the answer is “yes,” the more the opportunity belongs inside the company, or the more your existing stakeholders deserve a real stake in the upside. The more the answer is “no” — genuinely unrelated, developed independently, formally declined by the board — the more freedom you have to start fresh.

And before you finalize anything, walk through this checklist:

- Document the origin. When and how did the idea actually arise? Whose resources touched it?

- Take it to the board first. A formal disclosure and decision is the cleanest shield you can give yourself. Silence is the most expensive option.

- Default to keeping investors in the upside. Equity, warrants, royalties, participation rights — pick the instrument, but keep them riding the new value.

- Price the relationship, not just the equity. The points you “win” by cutting investors out are paid back with interest the next time you raise.

The Bottom Line

A pivot can be an exciting milestone in a founder’s life. It’s also one of the most dangerous, because it’s the rare decision where doing what feels obviously right for you can quietly transfer — or destroy — value that someone else paid for. Your investors took a risk on you when the outcome was uncertain. The way you handle the pivot is the clearest signal you’ll ever send about what kind of partner you are when the outcome finally arrives.

See it from their side of the table first. Then decide. You’ll make a better choice, and you’ll still be able to raise from those same people — and their friends — on your next company.

Sources:

- Guth v. Loft and the corporate opportunity doctrine: CaseMine

- Broz v. Cellular Information Systems: Studicata case brief

- Odeo buyback and Twitter outcome: TechCrunch

- Glitch-to-Slack pivot and investor handling: Startup Archive (Ben Horowitz)

Leave A Comment