A partnership does not require equity, and equity is never free.

Startup founders love strategic investors.

At least in theory.

A company that can help you sell, distribute, bundle, integrate, or get in front of the right customers sounds like the perfect investor. They bring capital and go-to-market leverage. They know the market. They have customers. They can accelerate the business.

All good.

But when a GTM partner says they want to invest, my first question is simple:

Why?

Not “why do we want their money?”

Why do they want to invest?

Because a business partnership does not require an equity investment. And sometimes the investment can create more strategic cost than strategic value.

That is the part founders need to be very careful about.

If one important company invests in you, what does that signal to everyone else in their ecosystem? What does it signal to their competitors? What does it signal to other potential customers, resellers, channel partners, platform partners, or acquirers?

I have seen this become a real issue.

One large customer or GTM partner invests. It feels like validation. It looks great in a press release. It creates momentum.

But then their competitors become less likely to work with you.

They wonder if you are neutral. They wonder if their data, roadmap, customer strategy, or competitive priorities are safe. They wonder if the investor will get preferential access. They wonder if buying from you means indirectly strengthening a competitor.

So the benefit of one strategic investor may come at the high cost of losing multiple other partners or customers. Some of them may be better for the business long-term.

That is why the “why” matters so much.

You can have a clean commercial agreement without touching the cap table:

“You resell our product, and we support your customers.”

“You introduce us to your enterprise accounts, and we give you a revenue share.”

“You bundle our technology into your platform, and we define pricing, support, and success metrics.”

None of that requires ownership.

So when a GTM partner wants to invest, founders should slow down and separate the two conversations:

- The commercial partnership.

- The equity investment.

They are related, but they are not the same thing.

The Real Question

The question I would ask any GTM partner who wants to invest is:

What does investing enable that a commercial partnership agreement does not?

That question cuts through the noise.

It forces everyone to get honest about motivation. And it forces the founder to think through the second-order effects.

A strategic investor is not just a source of capital. They are also a signal to the market.

Sometimes that signal helps.

Sometimes that signal hurts.

1. Financial Return

The cleanest answer is financial return.

They believe your company will become valuable, and they want exposure to the upside. Maybe they have a corporate venture arm. Maybe they have a balance sheet strategy. Maybe they believe your category is going to grow and they want to participate.

That is fine.

But then you should evaluate them like any other investor.

Are they value-add capital?

Will they help with future rounds?

Do they understand venture risk?

Are they investing on standard terms?

Will they be supportive if the company pivots, raises from their competitors, or sells to someone else?

The “financial return” answer is often the easiest to understand, but it is rarely the whole story. Big companies have many ways to put capital to work. If they are investing in you specifically, there is usually a strategic reason too.

And if there is a strategic reason, you need to know what it is.

2. Strategic Alignment

The second reason is strategic alignment.

They may believe that owning a small piece of the company creates deeper commitment between both sides. They may want to signal to their sales team, customers, board, or market that this partnership matters.

That can be positive.

Strategic capital can help validate a company. It can create executive attention. It can make the partner more invested in the success of the relationship.

But founders should be careful not to confuse symbolism with substance.

An investment does not guarantee sales.

It does not guarantee distribution.

It does not guarantee urgency.

It does not guarantee that their field team will care.

And it definitely does not guarantee that the rest of the market will see the relationship the way you want them to.

Your investor may describe the deal as “strategic alignment.”

Their competitors may see it as “you picked a side.”

That difference matters.

If the partnership matters, write down what matters.

Define the GTM plan. Define the sales motion. Define responsibilities. Define success metrics. Define timelines. Define what happens if nothing materializes.

Equity should not be a substitute for a real operating plan.

3. Strategic Control or Option Value

The third reason is the one founders need to examine most carefully.

Sometimes a strategic investor wants more than alignment. They want option value.

That can show up in several ways:

- Favorable commercial terms

- Exclusive rights

- Information rights

- Roadmap influence

- Restrictions on working with competitors

- Right of first refusal

- Acquisition positioning

- Market blocking

Some of these may be reasonable. Some may be dangerous.

The risk is that the investment quietly becomes a control mechanism.

A partner may not need to own much of your company to complicate your future. A small investment with the wrong rights can make future fundraising harder, limit your GTM flexibility, scare away other partners, or create friction in an acquisition process.

Founders often underestimate this.

The headline sounds great: “Strategic partner invests.”

But future investors may ask:

“Does this block you from working with others?”

“Do they have rights we should worry about?”

“Will their competitors avoid you?”

“Do they have access to sensitive information?”

“Could this create a problem in an M&A process?”

These are not theoretical questions. They matter.

The Hidden Cost: Market Neutrality

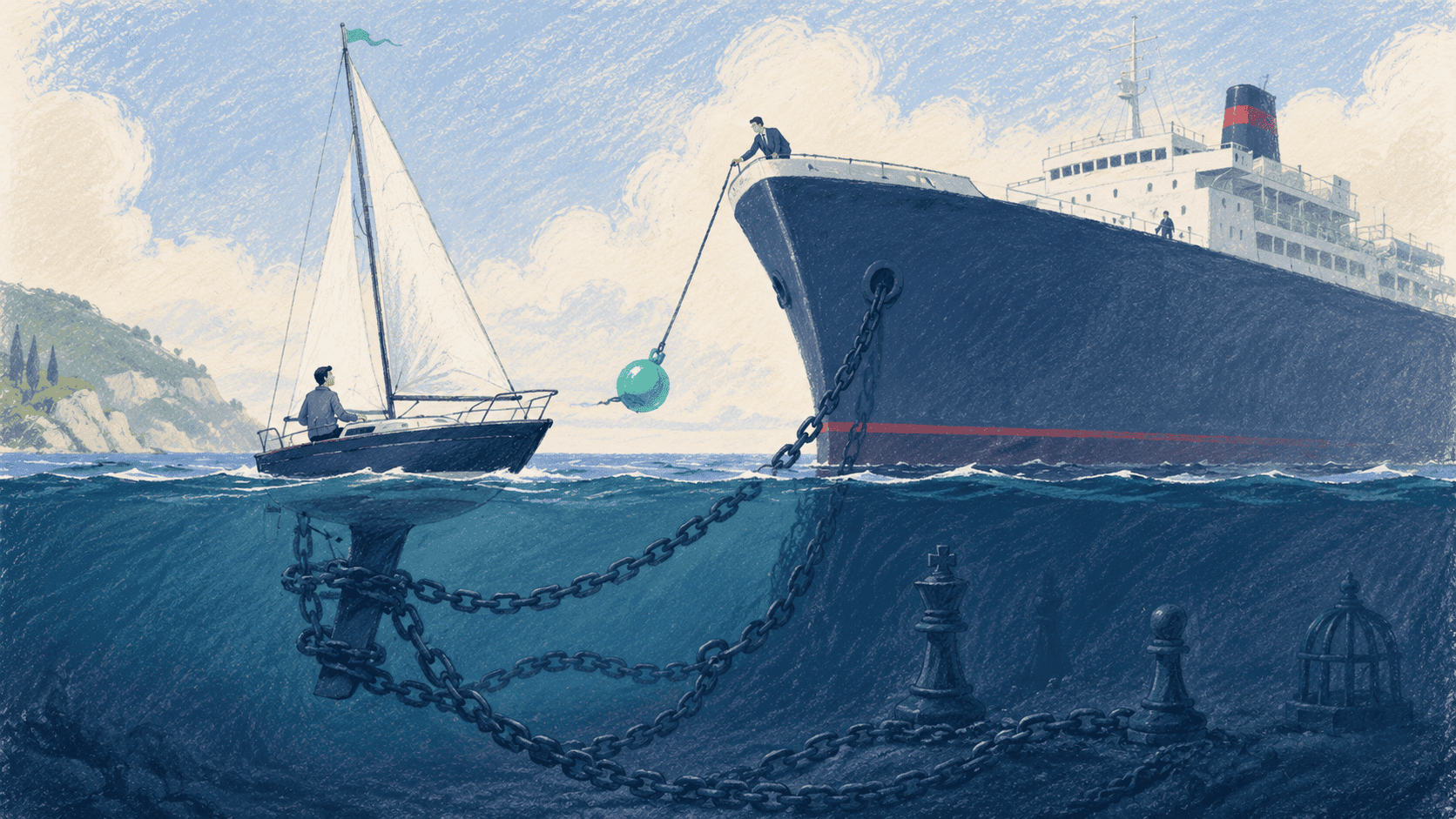

One of the biggest risks of strategic investment is losing market neutrality.

This is especially important if your company sells into an ecosystem with large incumbents, channel partners, platform companies, or potential acquirers.

If a major player invests, others may assume you are no longer neutral.

They may not say it directly.

They may still take the meeting.

They may still smile and say the relationship is interesting.

But they may slow-roll you, avoid deeper integration, limit data sharing, block internal sponsorship, or choose a weaker competitor because that competitor feels safer.

This can be very expensive.

You may gain one partner and lose five.

You may win one customer and make ten others uncomfortable.

You may get one powerful logo and accidentally narrow your future market.

That is not always a bad trade. Sometimes one strategic partner is so important that it is worth it.

But founders should make that trade knowingly.

Do not take strategic capital just because it feels validating.

Ask what it costs.

The Cap Table Sends a Message

Founders sometimes think of the cap table as private financial plumbing.

It is not.

Your cap table sends a message.

It tells future investors, partners, customers, employees, bankers, and acquirers something about your company.

If the investors are clean financial investors, the message is usually simple.

If the investors are strategic companies, the message is more complicated.

It may say:

“This company has strong industry validation.”

It may also say:

“This company may be aligned with one side of the market.”

Both can be true.

That is why the identity of the strategic investor matters. The terms matter. The competitive landscape matters. The timing matters. And the story you tell around the investment matters.

Keep the Two Deals Separate

The best way to stay clear is to separate the partnership from the investment.

The commercial deal should stand on its own.

If the GTM partnership makes sense, it should make sense without equity.

If the investment makes sense, it should make sense without vague promises of commercial magic.

That does not mean you should reject strategic investors. Some can be incredibly valuable. The right strategic investor can open doors, validate the market, improve product direction, and help the company scale faster.

But the terms need to be clean.

The motives need to be clear.

And the founder needs to understand what the investor is really buying.

The Founder’s Checklist

Before taking money from a GTM partner, ask:

- Why do they want to invest?

- What does the investment enable that a commercial agreement does not?

- Are they seeking financial return, strategic alignment, control, or option value?

- Will this make us look less neutral in the market?

- Will their competitors still want to buy from us?

- Will their competitors still want to partner with us?

- Could this scare away better customers or better GTM partners?

- Are there any exclusivity terms?

- Are there any restrictions on selling to or partnering with competitors?

- Are information rights appropriate and limited?

- Could this investment complicate future fundraising?

- Could this investment complicate M&A?

- Will other GTM partners view this as a conflict?

- Is there a real operating plan behind the partnership?

The most important one is still the simplest:

Why do they want to invest?

Founders should welcome strategic capital when it is transparent, aligned, and clean.

But do not let a partner use investment to get control they could not get through a normal commercial agreement.

And do not underestimate the cost of losing neutrality.

Capital is useful.

Distribution is useful.

Strategic alignment is useful.

But optionality is precious.

Protect it.

Leave A Comment